-1.jpg)

I remember back in 2017, when the Tax Cuts and Jobs Act eliminated tax-exempt advance refunding transactions at a projected savings of $16.8 billion in federal revenues. I had lunch with two other municipal quantitative bankers, and we discussed how unfair the act was because when issuers originally sold their bonds, they were under the impression that they could refinance their bonds any time prior to the bond’s call date– if markets improved.

This sparked our creativity to explore all of the fun ways to possibly still “advance refund” existing outstanding bonds.

A Look at Present Refunding Trends and Economic Influences

There were $50.8 billion in refundings in 2023 according to Bond Buyer. Most market experts expect 2024 municipal market issuance to increase in part due to the Fed cutting their rates, followed by municipal rates dropping and increasing the number of municipal bonds that could be refunded for cash flow savings.

Key Considerations:

- Due to the current U.S. economy, the Fed has delayed the start of the interest reductions.

- The calculations have not accounted for the possibility of utilizing the extraordinary optional call feature for Build America Bonds for refunding purposes (further details forthcoming).

- The observation that the gap between Treasury yields and municipal bond yields is widening has enhanced the financial attractiveness of the returns from refunding escrows, thereby boosting the economic viability of refunding transactions that involve escrows.

Revolutionizing Tax-Exempt Bond Refunding: Strategies for the Municipal Bond Market

It’s now 2024 and all those fun ways we thought of refunding outstanding tax-exempt bonds back in 2017 have come into play in the last few years but even more so recently.

Let’s take a look at some of the current ways to refund tax-exempt bonds:

Taxable Refundings of Tax-Exempt Bonds

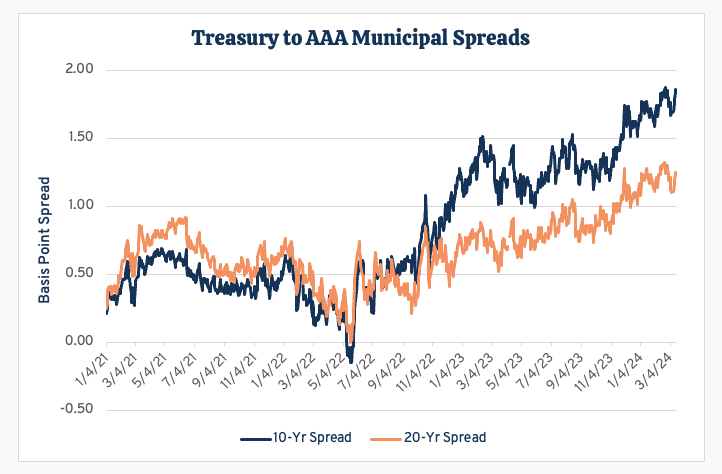

For this type of financing to be economically feasible, the markets would have to squeeze the differential between the taxable scales and tax-exempt scales to make any sense. As you can see from the graph below, from 2021 through 2022, the Treasury to Muni spread was very tight, thus making taxable refunding economically advantageous.

Another interesting possibility is to transition the taxable advance refunded bonds back to tax-exempt status once the original tax-exempt bonds that were refunded has been called.

This is permitted because once the original tax-exempt bond was actually replaced by the taxable advance refunding, there would no longer be any outstanding tax-exempt bonds on the originally financed project.

This allowed the issuer to then refund the taxable advance refunding bonds back to tax-exempt bonds without having two tax-exempt bond issues outstanding at one time. In most markets, the refunding of the taxable bond would produce savings.

Example: Advance Refunding of Taxable Advance Refunding Bonds

The issuer sold a bond deal in 2014. In 2021, they sell an advance refunding transaction that creates an escrow to pay off the 2014A bond debt service through 01/01/2024 and then pays off all the 2014A principal on 01/01/2024.

- 2014A Tax Exempt Bonds are callable in 01/01/2024

- 2021A Taxable escrow (funded with 2021A bond proceeds), pays off the 2014A Tax Exempt bonds P&I until 01/01/2024

- 2021A Taxable escrow refunds the 2014A Tax Exempt bonds on 01/01/2024

Part 2

- 2021A Taxable Bonds callable in 01/01/2031

- 2024A Tax Exempt escrow (funded with 2024A bond proceeds), pays off the 2021A Taxable bonds P&I until 01/01/2031

- 2024A escrow refunds the 2021A bonds on 01/01/2031

In the diagram below, the issuer pays the dark blue sections and the escrow pays the red sections.

.png?width=894&height=350&name=CHART-Advance%20Refunding%20%20(1).png)

Build America Bonds Refundings

When Build America Bonds (BABs)1 were issued, municipal issuers sold the bonds with either a make-whole calls provision or a standard 10-year call provision, since municipalities liked the flexibility of calling the bonds early for cash flow purposes.

|

Make-whole call provision: Allows the issuer to pay off the debt prior to its maturity date. When the issuer exercises the make-whole, they make a lump-sum payment to the investor. This payment is derived from a formula based on the net present value (NPV) of the future coupon payments and the principle that the investor would have received at today’s market price plus a small penalty adjustment. Standard 10-year call provision: Permits the issuer to “purchase” the bond back from the investor in the future at a predefined price. Extraordinary call provision: Also called an extraordinary redemption, is most commonly used when bond proceeds are not spent according to schedule or a catastrophe affects the financed project. |

Because of their repayment methodology, calling a make-whole bond early will not derive any savings to the issuer.

Since approximately 35% of the interest on a BABs was paid to the municipality through a federal subsidy, municipalities wanted to protect themselves should the federal subsidy not be delivered.

Municipalities did this by including an extraordinary optional call provision associated with BABs that should the federal government “change” the program, the municipality could use the extraordinary optional call provision to call the bond from the bondholder.

Various Build America Bond issues, due to the way the provision was written into the documents, had differing interpretations of what constituted a “change”.

For instance, if the federal government changed the percentage of interest it subsidized, some bond issuers could interpret this adjustment of subsidy as a “change" and execute the extraordinary call while others could not.

BABs Refunding in Action

In the recently decided case of Indiana Municipal Power Agency v. U.S., it was ruled “the spending cuts implemented by the Taxpayer Relief Act and the Budget Control Act are irreconcilable with section 1531’s 35% payment rate.

As a result, the Taxpayer Relief Act altered the Direct Payment BABs program, reducing the government’s payment obligation. When sequestration was implemented in 2013, the defendant was required by law to pay issuers of BABs a reduced rate.

This change was consistent with the basic principle that Congress is free to amend pre-existing laws.”

Essentially, the court ruled that the sequestration legislation amended section 1531, which in turn affected sections 54AA and 6431, significantly reducing the amount the federal government is required to pay by law to issuers of Direct Pay BABs. 2

The bottom line is most issuers with outstanding BABs, with the approval of their bond counsel, think they can now use the extraordinary optional call to refund the outstanding taxable BABs with tax-exempt bonds, saving them money.

*Note: The ability of issuers to actually use the extraordinary optional call is currently being contested. At this time (03/24/2024), investors of the Regents of the University of California's $1.1 billion outstanding Build America Bonds refunding3, which has priced but has not closed yet, hired a law firm and have told the university it must either pay bondholders more for the make-whole premium, cancel the deal, or face a lawsuit for breach of contract.

Tender Refundings

As discussed in detail in the Tender Offers: The Strategic Move in Bond Refunding blog, the issuer asks the bondholders if they would like to sell their bonds back to the issuer at a price.

If that purchase price is low enough, the issuer purchases the bonds using proceeds from a new tax-exempt bond where the new tax-exempt cash flow is lower than the refunded bond’s cash flow, producing cash flow savings.

Taxable Refundings

From 2021 through the end of 2022, the main methodology used by municipal issuers to advance refund outstanding debt was with taxable refundings.

This caused positive economic results because the spread between tax-exempt yields and taxable yields was tight. As the spreads widened, taxable refunding became less economical, the reason for the reduced number of taxable refundings compared to 2023.

Although I have seen some taxable refundings of tax-exempt bonds, they have been few and far between this year.

Tax-Exempt Refundings of Variable Bonds with Associated Swap

It was recently announced that an issuer with Midway Airport is looking into refunding variable rate debt associated with a commingled swap to allow the issuer to terminate the swap. (I do not have the swap documents, nor do I have the airport’s variable rate spread history to its swap index to analyze if this is being done for cash flow savings.)

"The Midway deal is day to day," Chicago Chief Financial Officer Jill Jaworski said, adding that Chicago is doing this refunding deal now because "market dynamics are favorable to terminate the associated swaps and issue fixed-rate refunding bonds."

"We believe taking out variable rate debt with fixed rate debt is prudent in managing [Midway]'s capital structure as it removes variable rate debt exposure," an S&P spokesperson said. "We view the terminations of these swaps as de-risking a portion of their debt portfolio and simplifying their capital structure."4

Forward Delivery Refundings

The following was recently discussed by an issuer but has yet to be executed:

Although issuers can no longer advance refund a bond (i.e., refund a bond that is callable greater than 90 days from execution) with tax-exempt bonds, they can get commitment from buyers to purchase refunding bonds in the future based on today’s rate plus a forward premium.

The forward premium depends on the duration of the commitment, specifically, the number of months remaining until the bonds eligible for refunding can be currently refunded. This includes the scenario where a bond can be called (or refunded) within 90 days or less from the time of execution.

The commitment by the future bondholder to purchase the bonds is usually less than one year and the forward premium can range from 4 basis points (bp) per month until the bond is callable to 15bp, depending on credit.

Conclusion

Issuers typically consider redeeming municipal bonds before maturity under two conditions:

- when bonds are initially priced to their call dates, often carrying coupons above market rates, known as premium bonds, or

- when bonds are issued during periods of high-interest rates.

This consideration becomes more pronounced when market interest rates decrease, making the financial conditions more attractive.

Although issuers currently cannot “advance” refund the bonds with tax-exempt refunds, there are other avenues they can explore to refinance the bonds and achieve either economic savings or meet other required objectives.

In conclusion, tax-exempt bond refunding is evolving, shaped by legislative changes and market dynamics, and has compelled issuers and financial professionals to innovate and adapt.

Despite challenges like the elimination of tax-exempt advance refunding and the fluctuating market conditions, the municipal bond market continues to explore and embrace novel refunding strategies.

Sources:

1 Build America Bonds (BABs) were introduced in 2009 as part of the American Recovery and Reinvestment Act (ARRA). These taxable municipal bonds featured issued by a municipality had initially 35% of the interest payment paid by the federal government making the bond’s interest rate to the issuer approximately equal to a bond had they issued it as a tax-exempt bond.

2 Federal Circuit Affirmed Claims Court on Build America Bonds (natlawreview.com)

3 Bond Buyer - Investors begin to challenge BABs redemptions - March 7, 2024

4 Bond Buyer - Midway Airport plans refunding deal that will terminate swaps – March 13, 2024

Related Municipal Finance Reading

- Bond Insurance: Making a Marketable Credit Better

- How Climate Risks are Shaping Municipal Financing

- Tender Offers: The Strategic Move in Bond Refunding

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)