The use of bond insurance has been increasing over the past six months. Currently, 10% - 12% of all primary municipal bond transactions have all, or a portion of, the bonds insured.

The key question is why are more municipal issuers selling their bonds in the primary market with bond insurance?

What is Bond Insurance?

Bond insurance is a type of insurance attached to a bond, purchased by either the issuer (primary market) or owner of the bond (secondary bond insurance), to improve the risk tolerance of the bond and allow the issuer to sell the bond at a lower yield.

If a bond is insured, the owner of the bond looks towards the bond insurance provider to guarantee the bond’s debt service payments (i.e., principal and interest payments) should the issuer be unable to make those payments.

Bond insurance does not eliminate the risk of an issuer default; it only shifts the risk to the insurer.

Bond insurance is usually available to investment grade issuers (i.e.,“BAA” market credit rating or better).

Since the bondholder is looking at the bond insurer as the “last line of defense” against non-payment of debt service, the bond carries the rating of the bond insurer and is priced based on the bond insurer’s rating.

The economic benefit of bond insurance for the issuer stems from the ability to sell the bond at a lower yield to the market, leveraging the bond insurer's high credit rating to compensate for the issuer's own lower rating.

Should the issuer not be able to make debt service payments, the bond insurer has the right to exercise the early payment option embedded in the insurance policy (i.e., collapse the transaction) if the related bonds are accelerated, either contractually or by operation of law.

History of Municipal Bond Insurance

A little history about municipal bond insurance:

- The first insured municipal bond was issued in 1971 through AMBAC.

- There were several major bond insurance companies (e.g., AMBAC, Assured Guaranty, Financial Guaranty Insurance Company), all with strong “AAA” ratings. In fact, no bond insurer had ever been downgraded from “AAA” until 2007.

- Through 2007, approximately 50-60% of all municipal bond transactions were insured.1

- When the financial crisis of 2007-2008 occurred, most bond insurance companies had large Collateralized Debt Obligations (CDO) portfolios, mortgage-backed security portfolios, and other structured finance products (e.g., derivatives) which quickly de-valued. The rating agencies re-rated the insurance companies based on their de-valued portfolios and downgraded them by multiple levels.

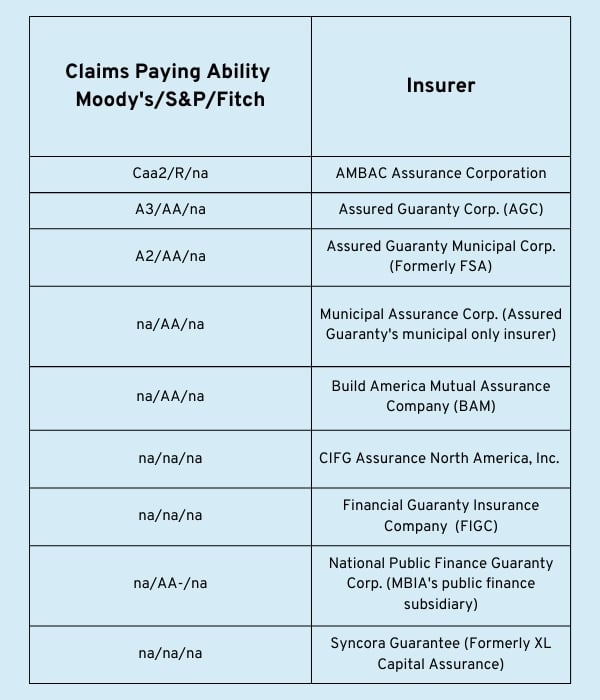

Below is a summary of the downgrades, all from “AAA”, that affected bond insurers post the 2007-2008 financial crisis:

After the downgrades of all the bond insurance companies’ ratings, the economics of bond insurance lost most of its value.

Current Major "AA" Rated Bond Insurers

Today, there are two main bond insurers, both rated “AA”: Assured Guaranty (AG) and Build America Mutual (BAM):

Assured Guaranty

Assured Guaranty is the leading provider of municipal bond insurance with approximately 61.3% of the market share ($19.5 billion) in 2023. AG consists of a group of insurance companies that includes Assured Guaranty Municipal Corp. (AGM) and Assured Guaranty Corp. (AGC).

Assured Guaranty has never defaulted on a principal and interest payment on time and in full – even when the issuer failed to pay.2

Assured Guaranty Ltd. (ticker symbol: AGO), is a publicly owned company subject to New York Stock Exchange and Securities and Exchange Commission regulation including disclosure, oversight, and transparency.

Build America Mutual

Build America Mutual was launched in 2012, in the wake of the financial crisis, as a muni-only, mutual insurer.

BAM’s mutual insurance structure means that its stakeholders – the municipal issuer-members who use insurance to reduce their borrowing costs and the investors who hold BAM-insured bonds – are aligned with a shared interest in accumulating capital and maintaining exceptional financial strength.

BAM’s capital is further protected by a unique 15% first-loss reinsurance treaty that covers losses of up to 15% of par on each policy.3

Calculating Bond Insurance Premiums

The methods for calculating and paying primary and secondary bond insurance premiums are:

Primary Bond Insurance

Primary bond insurance is usually paid with bond proceeds from the bond transaction being insured. The cost is calculated based on a percentage of the insured debt service payments (e.g., 0.25%).

There are two ways the bond insurance premium is calculated:

- On the delivery date of the bond transaction, the issuer wires the total cost of the premium, as calculated by the insurance company, to the bond insurer.

- The insurance premium is calculated annually based on the outstanding debt service at the point of the calculation and wired to the bond insurer. This methodology is rarely used for several reasons, one being that the issuer must come up with the annual insurance premium from their annual budget.

Secondary Bond Insurance

Secondary bond insurance premiums are paid by the current bondholder. Existing bondholders purchase secondary insurance to either lower the risk of non-payment, or potentially improve the value of the bond for trading purposes.

If the issuer is purchasing primary bond insurance and funding the insurance premium with bond proceeds, the Treasury permits the issuer to recover some of the cost of the insurance premium if the capital markets permit the issuer to earn a return on any invested bond proceeds at above the borrowing rate of bond transaction.

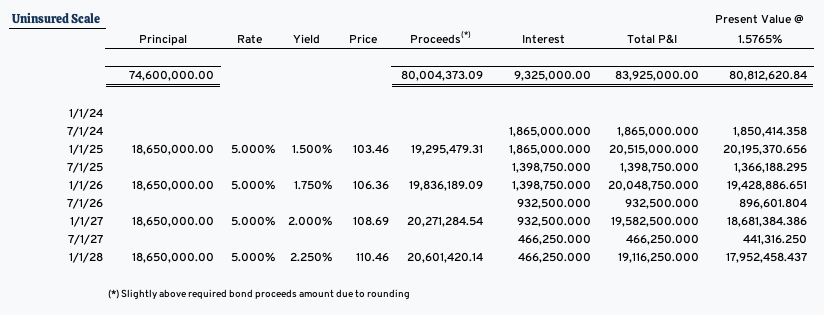

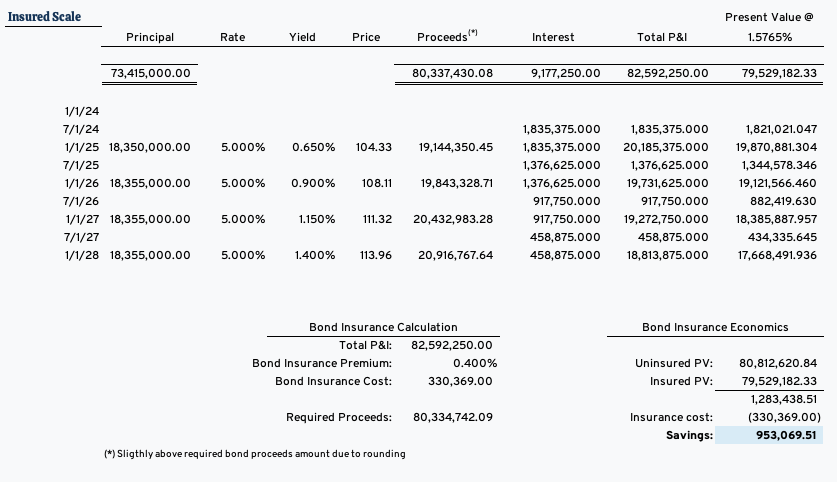

Cost-Benefit Analysis of Bond Insurance for an 'A' Rated Issuer

The example below shows the economics of an “A” rated issuer purchasing bond insurance for a bond transaction that must generate $80,000,000 in bond proceeds to finance the building of a new city hall and all expenses related to the financing. (The rate used for the present valuing calculations is a “blended” rate of the uninsured and insured bond scales.)

The bond insurance premium is assumed to be 0.40% of the total debt service paid at the delivery of the bonds.

In this case, you can see the yield was reduced by approximately 85 basis points for the insured transaction, even considering the additional bond proceeds needed to pay for the bond insurance, the issuer saved $953,069.

Note: The yields had to be reduced by a large amount due to the shortness of the analysis (4-year final maturity).

Conclusion

In summary, bond insurance can be used by both issuers (primary market) and bondholders (secondary market) to improve the credit risk of bonds and thus increase the value of the bond being sold in the capital markets.

Bond insurance does not eliminate the risk of lack of repayment of debt service–it redirects the risk from the issuer to the bond insurance company. Since bond insurance companies have sufficient capital and claims paying resources, the bond’s risk of non-payment is reduced.

Sources:

1 Oppenheimer – Municipal Basis Points – September 19, 2023

3 Build America Mutual is rated AA with a Stable outlook by S&P Global Ratings

Related Municipal Finance Reading

- How Climate Risks are Shaping Municipal Financing

- Tender Offers: The Strategic Move in Bond Refunding

- Capital Financing Delay Tactics for Issuers Facing High Interest Rates

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)