%20(6).jpg)

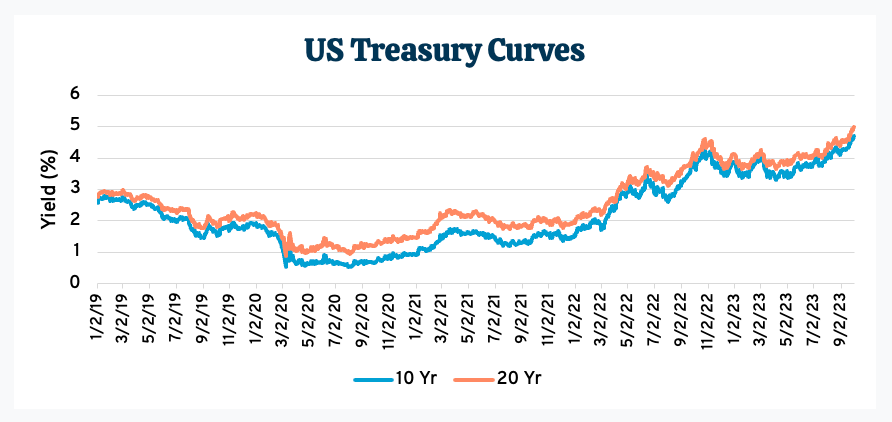

As the Fed continues to increase interest rates, municipal bond rates follow. This increase in rates, shown in the graph below, is making it much more costly for municipalities to finance capital projects.

As an example, assume an issuer financed a project with a $50 million bond financing structured as level debt service using 65% (tax-exempt adjustment) of the treasury yield curve (bonds sold as par bonds) with a final maturity of 30 years.

If the issuer sold the bonds on 03/02/2020 (a low point on the yield curve), the overall interest expense would have been $7.5 million. If the issuer sold the bonds on 09/29/2023 (a high point on the yield curve), the overall interest expense would have been $27.6 million.

That’s an additional $20.1 million of interest over the 30-year period.

Definition: Level Debt Service

A Maturity schedule in which the combined annual amount of Principal and Interest payments remains relatively constant over the life of a Bond Issue, according to the National Association of Bond Lawyers.

If an issuer wants to fund a capital project in a high interest environment, and (1) doesn’t want to lock in the high rates for the length of the financing (e.g., an average life of 15 years), and (2) expects interest rates to drop (i.e., incur interest rate risk), what are their options?

Below are six options a public sector issuer could consider when faced with high interest rates:

- Drawdown Programs

- Variable Rate Debt

- Commercial Paper

- Reimbursement Programs

- Direct Loan from a Bank

- Internal Banks

Before we discuss these options, let’s take a step back to discuss an alternative that is always the cheapest way to finance a capital project.

When I ran Citi’s Public Finance training program, I always started the first day with a question to the new analysts and associates: “What is the cheapest way to finance a municipal capital project?”

The analysts would usually answer tax-exempt fixed-rate bonds or variable-rate bonds. The actual answer is using 0% interest non-repayment money in the form of philanthropy (i.e., the thermometer counting donations in front of the library) or federal/state grants.

Access to this type of money is even more important in a high interest environment. Another source of “cheap” cash to finance projects is cash-on-hand that does not have to be reimbursed although the issuer loses the reinvestment potential of the cash.

Let’s look at the positives and negatives of each alternative borrowing option:

6 Capital Financing Delay Tactics for Debt Issuers

(1) Drawdown Programs – Borrowing money over a planned period

In most capital project financings, all the required bond proceeds are sold on the initial date of the debt service offering. The bond proceeds are then divided up into different accounts.

For example, most of the bond proceeds might be deposited in the “construction” account where it will be drawn by the issuer, through the trustee, when the fund is needed to pay construction expenses (e.g., contractor bills).

The issuer could delay a portion of the financing, hoping rates will drop, by setting up a drawdown program. In a drawdown program, the issuer sets up an agreement with an underwriter to sell bonds periodically (e.g., monthly or semi-annually) over a set period of time.

Benefits of a drawdown program:

- The issuer receives enough bond proceeds periodically to meet their current expenses until the next financing.

- This structure also shortens the life of the overall debt obligation.

Negatives of a drawdown program:

- If interest rates continue to increase, the issuer will be selling the future bonds in a higher interest rate environment.

- The buyers of the bond will require a higher yield because there is the added risk that the issuer will not be able to sell bonds in the future and the project completion could come into question.

(2) Variable Rate Bonds – Borrowing for long periods with short-term interest rates

In my previous blog, “Variable Rate Debt – the Good, the Bad, the Flexibility,” I discuss the two types of variable rate bonds.

One is sold in higher increments and can be returned to the issuer if the bondholder is not in favor of the new interest rate, while the other is sold in smaller increments and cannot be returned to the bondholder.

Benefits of variable rate bonds:

- Variable rate debt can have the flexibility of allowing the issuer to refinance the debt into fixed-rate debt in the future when interest rates have decreased.

- Additionally, an issuer, such as a university, state, or city, can finance a portion of their capital project with a variable rate and finance the rest with a fixed rate.

Negatives of variable rate bonds:

- Since the interest rate is not set on the bond at the original issue but changes periodically based on an index plus a spread, interest rate risk can be driven by market moves. This means the issuer must estimate the interest expense when analyzing their budget.

- Also, since the interest rates are not locked in, the interest expense on the project can continue to go up.

- There may not come a time when long-term fixed rates are attractive enough to refinance the variable rate debt and if variable rates increase, the completion of the financing of the project might become a budgetary issue.

(3) Commercial Paper – Borrow in the short-term market with commercial paper (CP)

Through an offering memorandum, the issuer specifies the maximum amount of commercial paper that will be outstanding at any time (e.g., $300 million).

The issuer then issues a portion of the maximum amount of CP to finance the expenses of the project. The issuer can issue CP notes whenever they need money up until they hit the maximum amount. CP notes have a maximum maturity of 270 days, but the issuer can choose a CP maturity before 270 days (e.g., 30 days) based on market rates when the CP note is issued. This means that at any time, there could be multiple CP notes outstanding with different maturity dates.

Anytime CP notes mature, the issuer can remarket the CP notes back to the market with any maturity from 1 to 270 days. The issuer can continue to re-market the CP until it is refinanced with fixed-rate bonds.

Refinancing commercial paper is a method an issuer might choose when long-term interest rates decrease. When setting up a CP program, the issuer needs both a remarketing agent and usually needs to enter into a bank’s standby letter-of-credit, both adding to the cost of issuing CP.

Benefits of commercial paper:

- Since it is a variable rate instrument, commercial paper has all the same benefits and drawbacks as variable rate bonds I mentioned above, along with other risks.

The two additional negatives of commercial paper:

- Unpredictable market conditions could make remarketing the CP notes challenging.

- The CP could be priced at a higher interest rate than if it were issued as long-term fixed rate bonds.

(4) Reimbursement Programs – Use internal funds to finance the project with the plan to reimburse the expense in the future

When an issuer finances a project with their current available cash, they must specify how they plan to reimburse themselves in the future. There are 3 requirements the issuer must meet to issue reimbursement bonds:

The issuer must adopt an official intent that the original expenditures will be reimbursed with tax-exempt bond proceeds.

- The reimbursement allocation must be made not later than 18 months after:

- The date the original expenditure is paid, OR

- The date the project is either placed in service or abandoned

However, in no event may the reimbursement allocation be made more than three years after the date the original expenditure is paid.

B. The original expenditures, subject to reimbursement, must be one of the following:

-

- Capital expenditures

- Costs of issuance

- Certain extraordinary working capital expenditures incurred before the issuance of the reimbursement bond

- Grants (as defined in Treas. Reg. section 1.148-6(d)(4))

- Qualified student loans (as described in IRC section 144(b))

- Qualified mortgage loans (as described in IRC section 143(a))r

- Qualified veterans’ mortgage loans (as described in IRC section 143(b))

Benefits of reimbursement programs:

- A reimbursement bond gives the issuer the ability to delay locking into long-term fixed rate rates from 18 to 36 months, possibly allowing long-term fixed rates to decrease.

Negatives of reimbursement programs:

- Since reimbursement financing requires current cash in control by the issuer, the issuer will lose the reinvestment earnings on the cash until the money is reimbursed.

- If fixed-rate interest rates increase, the overall cost of the project has the potential of going up compared to just issuing fixed-rate long term bonds originally.

(5) Direct Loan from a Bank – Borrow from a bank with a plan to refinance in the future

If available, issuers can obtain an interim loan from a bank where the total loan amount is set, and the issuer “withdraws” from the loan when the expense must be paid.

At some time in the future, the issuer can refinance the loan with long-term fixed-rate bond proceeds.

Benefits of a Direct Loan:

- This type of financing can have less administrative burden than other delay financing techniques if the bank requires less documentation.

Negatives of a Direct Loan:

- The borrowing rate is set by the bank and not the open market which may lead to a generally higher borrowing rate. Unlike other delay financing techniques, if interest rates don’t decrease, this technique might end up costing the issuer more than originally selling long-term fixed-rate bonds.

(6) Internal Banks – Borrowing money from within the entity

Many issuers have cash on hand that is not dedicated to a specific use but acts more like a reserve. That money usually sits in a daily bank account, earning a low interest rate.

The client could use that money to finance all or a portion of the project instead of issuing high-interest rate bonds (depending on the market).

Benefits of Internal Banks:

- In theory, the public sector entity could save the difference between what they would have borrowed and owed in interest and could see a higher return on the money than it would by sitting in a bank account with a low yield.

Negatives of Internal Banks:

- The issuer could lose money if the bank's interest rate goes above the hypothetical fixed-rate long-term borrowing rate the issuer could have initially locked into.

Delayed Issuance Example

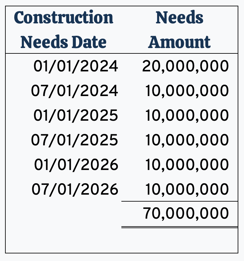

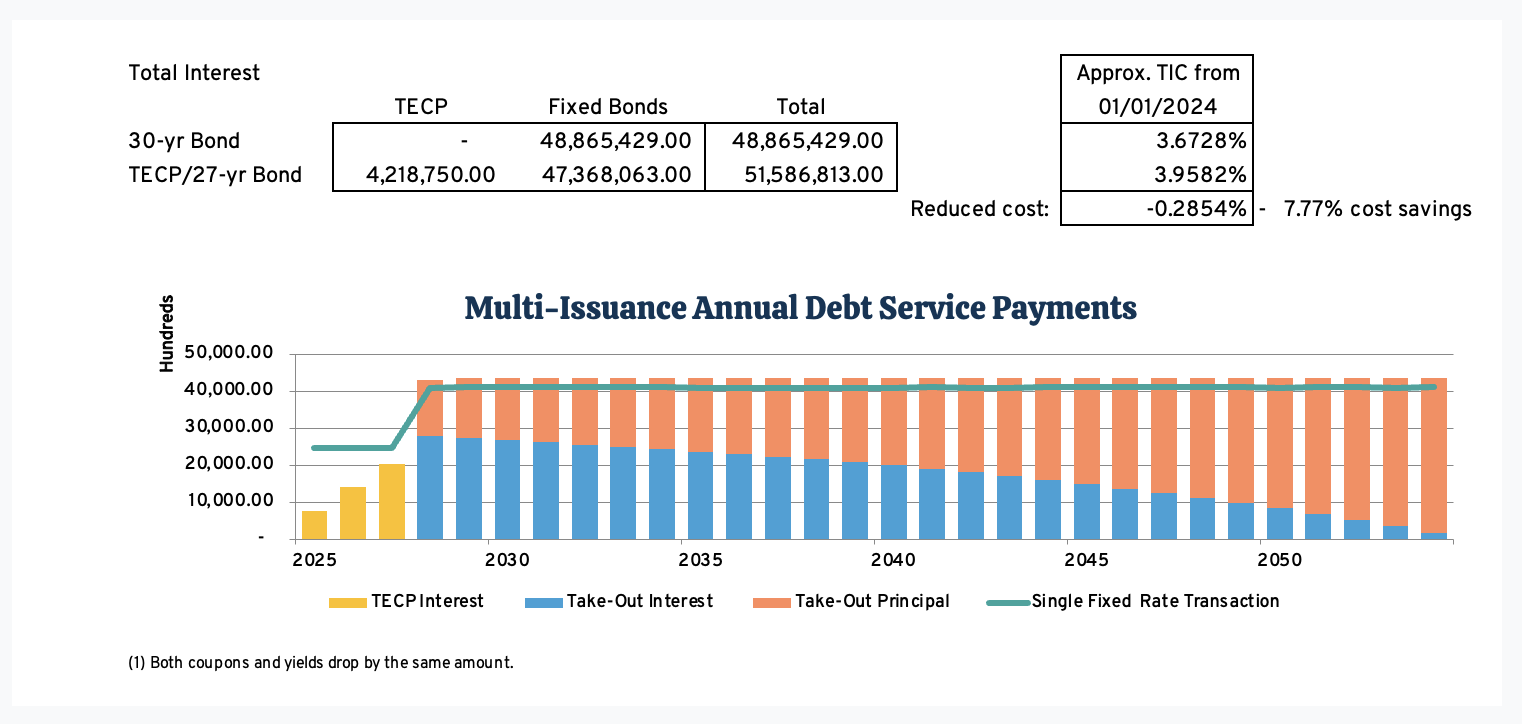

To show the possible benefits/disadvantages of a delayed issuance option, below is an example that compares selling a 30-Year bond issuance 01/01/2024 to issuing tax-exempt commercial paper (TECP) for three years, and then remarketing the TECP with a 27-Year bond issuance.

General Financing Assumptions:

(1) Issuer needs $70,000,000 in construction needs as displayed below

(2) Using 9/8/2023 "AAA" MMD curve, all bonds sold at par

(3) Assuming TECP rate of 2.50%, LOC of .50% and remarketing of 0.125% until fixed bond take-out

(4) All issues have equal general cost

(5) For single financings, construction draw account earning 1.5% until drawn

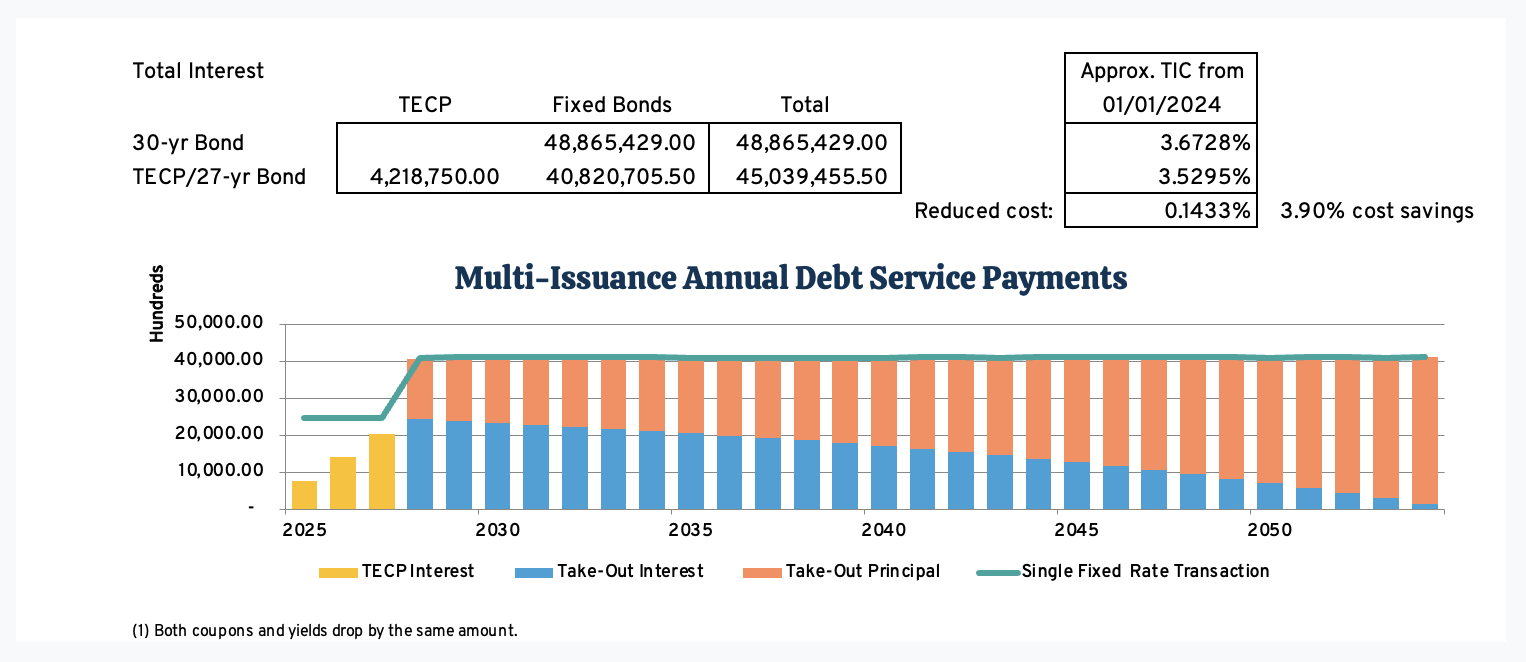

Scenario 1: Rates (1) remain constant when selling the take-out financing versus single 30-Yr issuance

Scenario 2: Rates (1) drop 50.00bp when selling the take-out financing versus single 30-Yr issuance

The 50.00bp drop in long-term fixed-rate interest rates 3 years after the initial issuance date is equivalent to saving $10,185,737 in interest expense over the life of the financing, or an interest savings of 20.84%.

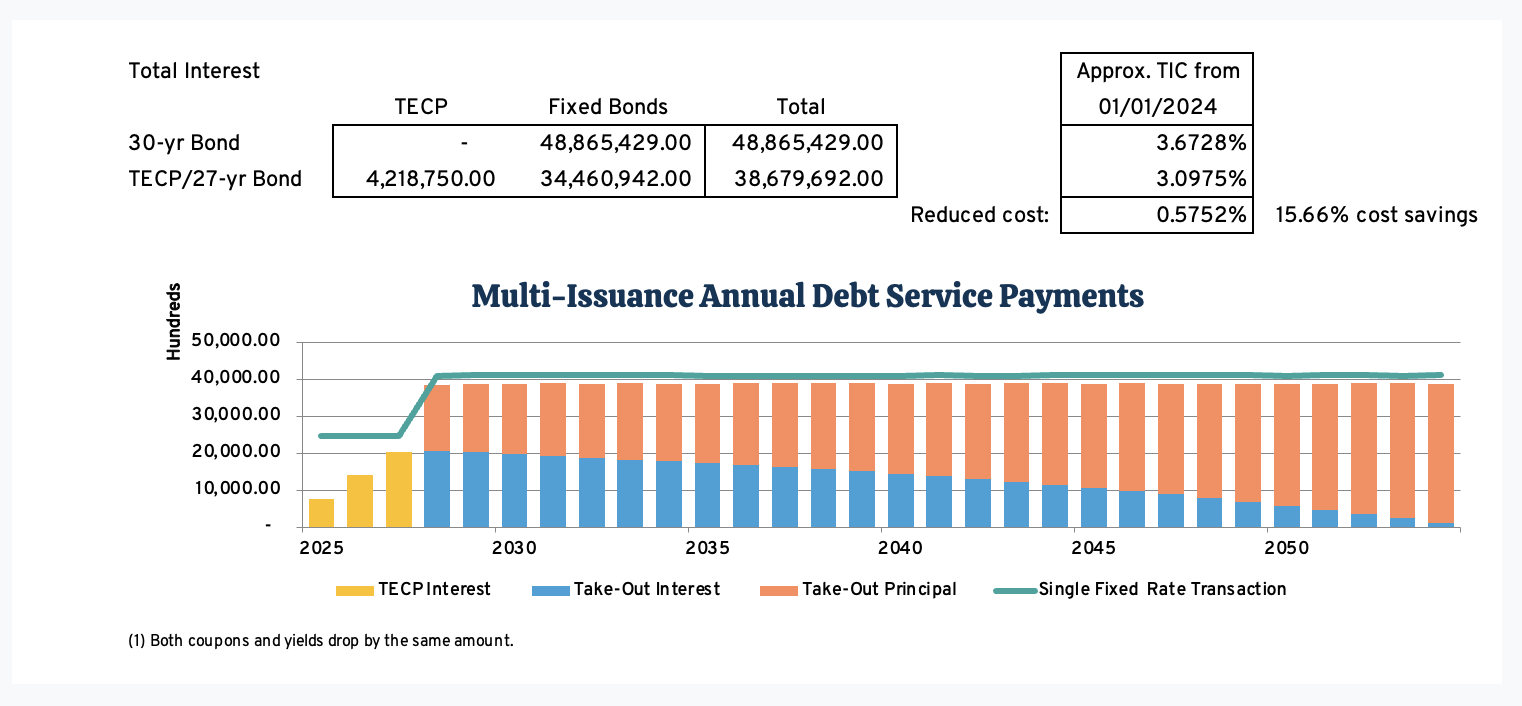

Scenario 3: Rates (1) increase by 50.00bp when selling the take-out financing versus single 30-Yr issuance

The 50.00bp increase in long-term fixed-rate interest rates 3 years after the initial issuance date is equivalent to saving -$2,721,384 in interest expense over the life of the financing, or an interest savings of -5.57%.

Conclusion

There are several ways to delay the selling of long-term fixed rate bonds in a high interest rate environment. None of the methods are bulletproof and most require the issuer to sell bonds in the future.

If interest rates decreased in the future compared to today, the issuer’s overall cost of the financing would be lower (including the period where the issuer sold potentially cheaper variable rate debt until they refinanced the variable with long-term fixed rate bonds).

However, if long-term fixed rate interest rates continued to increase, as did short-term variable rates, the overall cost of the project would be more expensive than initially planned.

Also note that some of the delay financing methods add additional administrative burdens and potential additional expenses (e.g., remarketing fee costs).

Related Municipal Finance Reading

- DebtBook's Premium/Discount Amortization Methodology Explained

- Advance Refundings - The Muni Gamble

- A 'Game Changer' for the City of Memphis, TN

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)