Variable rate debt, also known as Municipal Variable Rate Securities, allows an organization to borrow money for long periods of time while paying short-term interest rates to investors. These obligations have a long-term nominal maturity, which bears interest at variable rates adjusted at predetermined intervals. The two main types of variable rate bonds are (1) Variable Rate Demand Obligations (VRDOs) and (2) Floating Rate Notes (FRNs).

Both types of variable rate bonds are floating rate obligations issued by the public sector, but they each present benefits and disadvantages to the issuer and bondholder.

One is sold in higher increments and can be returned to the issuer if the bondholder is not in favor of the new interest rate, while the other is sold in smaller increments and cannot be returned to the bondholder.

If an issuer, such as a university, state, or city, is drawn to the benefits of a variable rate bond, they can finance a portion of their capital project with a variable rate and finance the rest with a fixed rate.

Let’s dive into the differences, benefits, and drawbacks of VRDOs and FRNs to help you understand why they are used in the public sector.

Variable Rate Demand Obligations (VRDOs)

VRDOs are floating rate obligations that are sold in increments of $100,000 with a periodic interest rate reset. The interest rate can be changed daily, weekly, or monthly by a remarketing agent. These obligations are then remarketed priced at par. Bondholders can “return” the bond to the issuer if they do not like the reset interest rate.

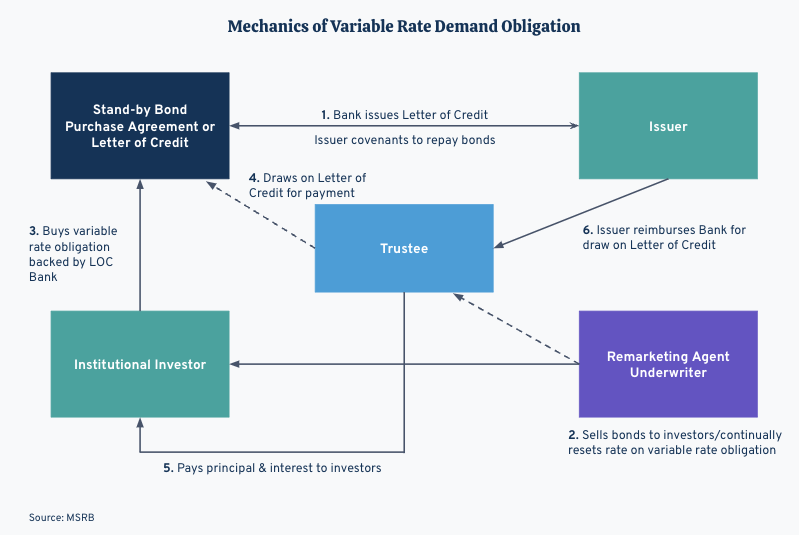

In order to have a mechanism to repurchase the obligation if the bondholder should chose to return it, most issuers purchase a liquidity agreement, which is a stand-by bond purchase letter of credit agreement (LOC) from a bank; or an issuer can set up a self-liquidity mechanism. Once the obligation is repurchased, the issuer resells the obligation back into the market.

The image below, from MSRB, displays the mechanics of a variable rate demand obligation.

Floating Rate Notes (FRNs)

FRNs are floating rate obligations that are sold in increments of $5,000 and the interest rate is set to a variable index plus a spread. In the public sector, this rate comes from the SIFMA (Municipal Market Swap Index). The bondholders do not have the ability to put (i.e., return) the bonds back to the issuer at any time.

This means FRNs do not require either a remarketing agent or a liquidity tool (i.e., backup bank LOC). The interest rate is set periodically based on the base index plus a spread.

According to MSRB, FRNs are not generally subject to optional redemption until the end of the floating rate period or six months prior to the maturity date at a purchase price of par plus accrued interest if optional redemption is permitted.

If the bonds are unable to be remarketed at the end of a floating rate note period, the interest rate may increase. And after a specified period, the interest rate can increase to the maximum value until the FRNs are resold (soft put). The maximum interest rate has generally ranged from 9 percent per annum to 15 percent per annum.

Alternatively, if the bonds are unable to be remarketed or refinanced at the end of the floating rate note period, the issuer may be obligated to fund the full amount of the purchase price of the tendered FRNs (hard put).

How is the Interest Rate Set for Variable Rate Debt?

The variable rate paid by the issuer to the bondholder is set periodically and is based on the definition in the Official Statement.

As an example, the interest rate on the bond can be set on the first Wednesday of every month and the interest is paid semi-annually on both January 1 and July 1 of each year. Transactions can have different rate reset periods that happen the first Wednesday of every month or every Wednesday. They can also have interest payment periods on the first Wednesday of the month or every Wednesday that are monthly or semi-annually.

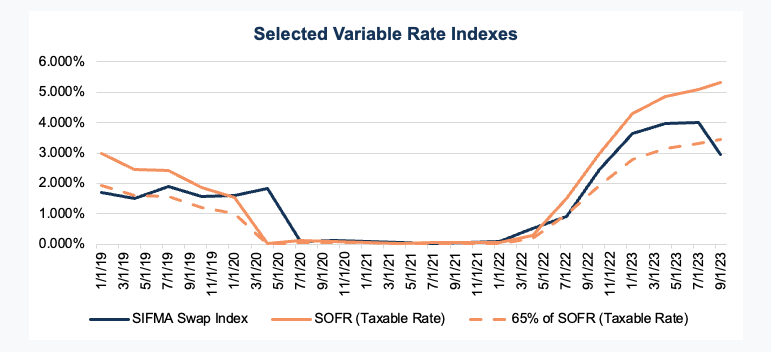

The interest rate can be set by benchmarking the rate to a short-term index plus a specified spread. For tax-exempt bonds, the index is usually either:

(1) SIFMA plus a spread or

(2) A percentage (e.g., 65%) of Secured Overnight Financing Rate (SOFR) plus a spread.

Fixed-Rate Municipal Bonds vs. Municipal Variable Rate Bonds

When an issuer finances a capital project, they have many ways to access capital. The most used methodology is to borrow money from the capital markets using fixed-rate bonds.

Fixed-rate bonds provide these benefits to issuers:

- The ability to budget for exactly the amount of principal and interest that is due in the upcoming fiscal year, since the borrowing cost is locked in.

- No additional maintenance is required on the bonds (e.g., remarketing the bonds), except for the actual payments made to the bondholders and issuing standard disclosure documentation.

Another way issuers can finance capital projects is by issuing variable rate debt. Variable rate debt brings the following drawbacks to the issuer:

- Introduces interest rate risk into the financing costs and indirectly into the budget process.

- Not knowing, on the date of delivery, how much interest they will have to pay over the life of the financing.

- Continued maintenance of the bonds in the form of:

- Resetting the interest rate on the bonds periodically.

- Finding new buyers of the variable bonds should the existing bondholder no longer wish to own the bonds.

- Hiring and paying a remarketing agent throughout the life of the financing.

The Benefits of Issuing Municipal Variable Rate Securities

If issuers are aware of the drawbacks variable rate securities bring, why would issuers choose to finance capital projects by issuing variable rate debt instead of fixed-rate date? Here are 3 reasons municipal bond issuers opt for a variable rate:

1. Potential to Lower Costs

Selling variable rate debt can potentially lower the cost of the capital project’s financing. Since the interest rates on variable rate bonds are set periodically (e.g., monthly), the interest rates are based on short-term rates, which are usually lower than long-term rates, saving the issuer money.

(Note: in an inverted yield environment, as we’re seeing in 2023, short-term rates are higher than long-term rates.)

Variable rate debt can be used to finance a capital project in three ways:

- Variable rate debt can be issued to finance either the total project or a portion of the project (e.g., 10% - 15%), with the remainder financed with fixed-rate debt.

- Issue “multi-modal” bonds which allows the issuer to change the interest rate or other terms of the bond over time. They are called “multi-modal” because they have multiple modes or options for the interest rate.

For example, multi-model public debt might start with a fixed interest rate and then switch to a variable interest rate after a certain period of time. How and when the issuer can change the mode of the bond is defined in the Official Statement. - Maintain financing flexibility with variable rate debt. Issuers can elect to pay off or refinance variable rate debt at any time in the future. Variable rate bonds are “callable” at any time at par.

This flexibility allows the issuer to sell variable rate bonds in a high fixed-rate environment when they need the proceeds, even though interest rates are considered high, and fix the variable-rate bonds out in the future when interest rates decrease.

2. Hedge a Liquidity Position

If the issuer has cash invested in a daily investment vehicle, they can set up a “non-perfect” hedge using variable rate debt. The daily investment rate goes up and down based on the current markets.

Variable rate debt has the same property. If interest rates increase, the issuer will earn more on their daily investments, but at the same time, the issuer will have to pay more in variable rate interest. If interest rates decrease, the issuer will pay less variable rate interest at the same time they are earning less on their daily investments.

Although both the daily investment and the issuer's variable rate interest cost might increase or decrease based on different factors, they both typically move in the same direction making the variable debt a hedge to the liquidity position.

3. “Variable-to-Fixed” Rate Swap

A “variable-to-fixed rate” swap is a contractual agreement under which two parties agree to exchange interest rate payment obligations for a specific notional amount for a specific period of time.

Issuers enter “variable-to-fixed” rate swap because, over the life of the financing, the issuer believes (1) the cost of the financing will be cheaper than if they issued fixed rate bonds and (2) wants to eliminate uncertainty of interest payments in the budget. In a “variable-to-fixed” rate swap financing:

- The issuer sells variable rate bonds in the capital markets.

- The issuer enters into an agreement with a counterparty to pay them a fixed rate interest amount on a set dollar amount in exchange for receiving a variable rate interest amount on the same set amount.

(Note: the index the issuer is using to calculate the variable rate interest paid to the bondholder is sometimes a different index than the interest rate they are receiving from the counterparty).

The economic analysis of a swap is complicated but when entering into a swap, the issuer believes that the fixed rate of the swap will always be cheaper to the issuer than if the issuer initially sold fixed-rate bonds.

Variable Rate Debt Usage in Today’s Markets

The diagram below shows several variable rate indexes used to price variable rate bonds. (Remember: an issuer’s credit quality helps define different adjustments to the index (e.g., 65% of SOFR + 25 basis points (bp))

Note: In the three diagrams below, All cash flows are structured annually, and all present valuing is back to year 0.

Many issuers refinanced their variable rate debt while fixed-rate bonds were at historical lows in recent years. However, as the Fed has been increasing interest rates, making it harder for municipalities to finance projects with fixed-rate long-term debt, several issuers have been using the strategy of financing with variable rate debt (even though short-term variable rates are high) with the hopes that long-term fixed-rates will decrease in the future, and they can refinance in lower interest environments.

As a simple example, a municipality has to sell $50,000,000 in bonds to finance a project (includes the cost of issuance expenses). Below are two examples of financing plans:

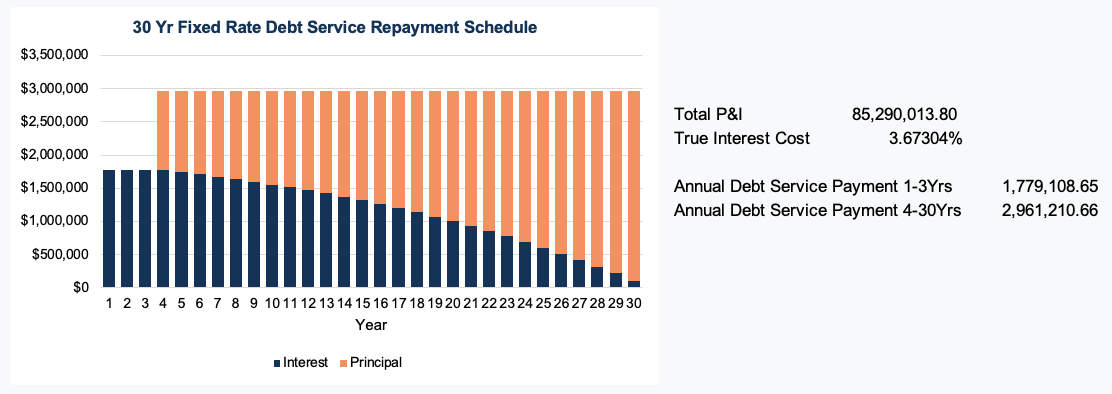

Example 1: 30-Year Fixed-Rate Debt Financing Plan

Using the 9/8/2023 MMD AAA curve (straight line interpolating for the missing years), sell fixed-rate bonds maturing from year 4 to year 30, structuring the debt as annual level debt with all bonds being sold at par. The debt would have the following characteristics seen in the chart below:

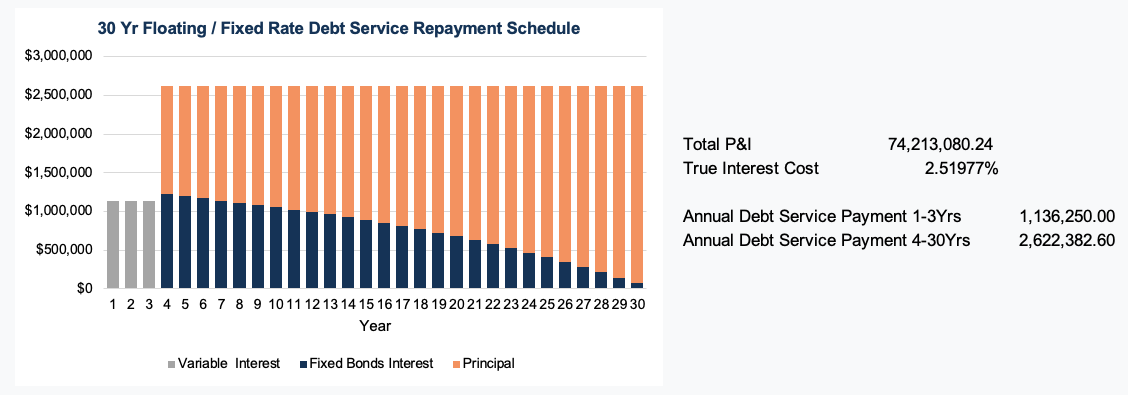

Example 2: 30-Year Floating/Fixed-Rate Debt Financing Plan

Initially sell variable rate debt with a plan to refinance in 3 years at an average rate of 2.00% with a letter-of-credit cost of .25%. After 3 years, restructure the variable rate debt with fixed-rate long-term bonds using the 9/8/2023 MMD AAA curve less 100bp (assuming market improvement) on each coupon, and maturing the bonds from year 1 to year 27 structured as level debt with the bonds sold at par.

In the analysis, we assumed $500,000 in additional costs (i.e., underwriters discount & cost of issuance) when issuing the fixed-rate long-term bonds. The overall financing would have the following characteristics:

It is important to note that if fixed-rate long-term coupons increase after three years, the issuer has the option to keep the debt in variable rate mode and wait until the fixed-rate long-term market improves. However, the variable rate market rates could also increase, and the cost of the overall financing might have been cheaper if the issuer initially just issued fixed-rate long-term bonds.

In this analysis, if you wanted to calculate the breakeven true interest cost of (1) the variable bonds 3 years at 2.00% (includes remarketing fee) plus a .25% letter-of-credit fee refinanced with fixed-rate bonds compared to (2) originally issuing only fixed-rate bonds, the fixed-rate long-term bond coupons on the refinancing bonds could have increased by 45bp and the overall true interest cost of both financings would have been identical.

Risk vs Reward: Financing Capital Projects with Variable Rate Debt

To summarize, variable rate debt can be used to meet several different issuer’s objectives. Variable rate debt can be used to:

- Lower the cost of financing

- Offset other assets’ earnings inconsistencies

- Be part of an overall financing strategy

Unlike fixed-rate long-term debt, variable rate debt always comes with interest rate risk. The risk can be driven by market moves due to general market sentiment, an issuer credit event, or an unexpected world event. If there is a downturn in the market the risk to issuers can lead to increased borrowing costs which will affect their budgets.

DebtBook's Variable Rate Debt Management

DebtBook’s Variable Rate feature is built specifically to help treasury teams manage variable rate debt. As part of our Debt Management offering, we make it easy to stay on top of your obligations with dynamic tools designed to save time and improve accuracy.

-

Dynamic Rate Calculations: Automatically generate variable rate debt reset rates leveraging market data integrations.

-

Payment Management: Clearly and accurately identify interest due for each reset and payment period as well as liquidity and remarketing fees.

-

Market Benchmarking: Track variable rate debt performance against indices relevant to municipal borrowing like SIFMA and SOFR.

-

Predictive Insights & Scenario Analysis: Forecast future rate changes and assess financial impact using historical trends and market conditions.

-

Compliance & Audit Readiness: Maintain a complete audit trail with historical reset rates, payment calculations, and variance tracking.

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)