The main benefit of fixed-rate debt to the borrower is that they can easily budget for future interest payments because they know the interest amounts they will pay to investors and on what dates they will make those payments.

There are four types of fixed-rate bonds that can be issued:

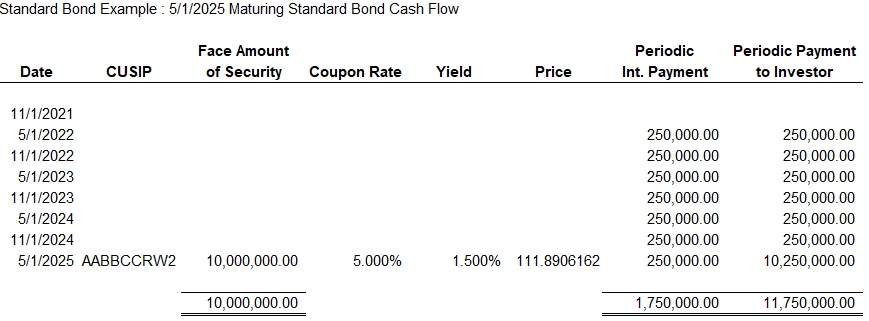

- Current interest bonds pay investors periodic interest payments throughout the bond’s life. These payments are based on the bond’s principal amount and interest rate. On the security’s maturity date, the principal amount is returned to the investor along with the final interest payment. Below is a sample of a standard current interest bond’s cash flow:

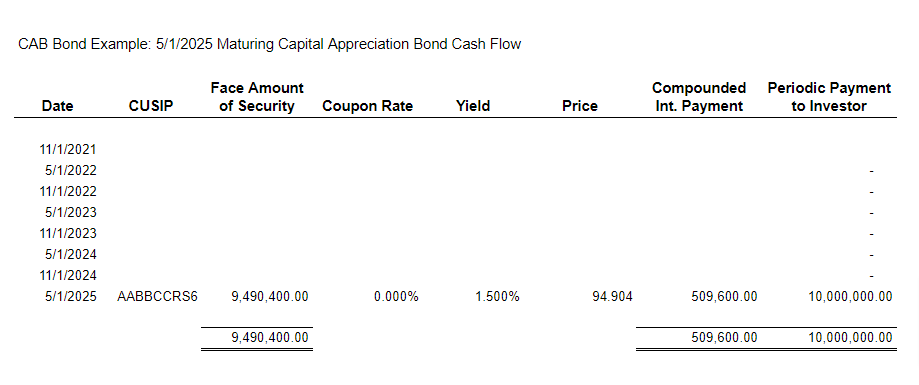

Most standard bonds are sold in increments of $5,000. Private placement bonds are sold in increments of $5,000 to $100,000. Bonds have also been sold in $1,000 increments to maximize their availability to borrowers. In some instances, bank loans may be sold in increments as little as $1.00 or $0.01. - Capital Appreciation Bonds (CABs) are securities purchased at a deep discount in multiples of $5,000, and pay the investor no physical interest until the final maturity date. On that date, the investor receives a single payment (called the “maturity value”) representing the initial principal amount and the total investment return. CABs are distinct from traditional zero-coupon bonds because the investment return is considered compounded interest instead of accreted original issue discount (OID). Only a CAB’s initial principal amount would be counted against a municipal issuer’s statutory debt limit. This is unlike a traditional zero-coupon bond, which counts the total par value. Below is a sample of a CAB’s cash flow:

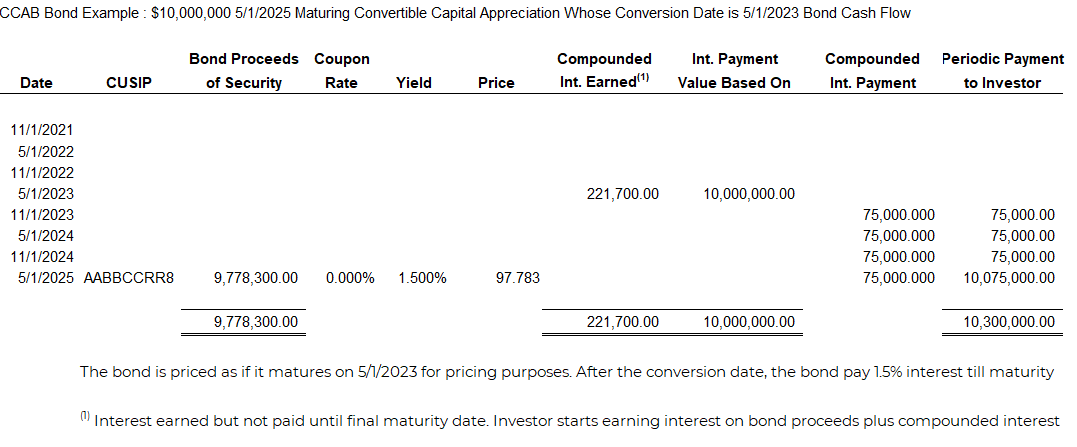

- Convertible Capital Appreciation Bonds (CCABs) are long-term municipal securities on which the investment return on an initial principal amount is assumed to be reinvested at a stated compounded rate until the conversion date. After the conversion date, the investor starts receiving periodic interest payments on the original principal amount plus the compounded value of the security through the conversion date. At maturity, the investor receives the initial principal amount, the compounded value through the conversion date, and the interest payment. Below is a sample of a CCAB’s cash flow:

- Stepped Coupon Bonds (SCBs) have the same cash flow traits as standard bonds, but the interest rate changes at either a specified date or periodically over time. Below is a sample of a stepped coupon bond’s cash flow:

What’s important here?

By issuing fixed-rate debt, an issuer can forecast and budget how much cash it will need to pay out and when. To accurately plan future cash outlays, it’s important to understand which type of fixed-rate bond is being issued and the important dates associated with it.