.jpg)

The easiest way to explain the economic advantage of a tax-exempt bond is that the owner of the bond does not have to pay income taxes on the interest of the bond. But there are more “layers of the onion.”

Below we discuss some issues to consider when determining the economics of a tax-exempt bond.

Factors to Consider for Tax-Exempt Bonds

1. The issuer of the bond

The issuer of the bond is important because depending on the location of the issuer, the buyer of the bond might not have to pay (1) federal taxes, (2) state taxes or (3) local taxes on the bond.

However, just because a bond is tax-exempt does not mean the bond is “triple” tax-exempt to the buyer.

For example, if the City of Martinville, New York issues a tax-exempt bond and the buyer of that bond lives in City of Martinville, the buyer of the bond would receive “triple” tax-exemption (federal, state and city (if any)) from their income taxes.

However, if the buyer of the bond lives in Provo, Utah, the buyer would only receive federal tax-exemption, not state tax or local tax exemption.

2. The bond buyer's federal tax bracket

Tax brackets for Americans vary depending on income level.

For the tax year 2022, the federal income tax brackets range from 10% to 37%.

3. The state the bond buyer lives in and their state tax bracket

State tax brackets depend on the filing status, income level, deductions, credits, and other factors.

42 states and the District of Columbia levy individual income taxes. Of those states taxing income, 11 have single-rate tax structures, with one rate applying to all taxable income.

Conversely, 30 states and the District of Columbia levy graduated-rate income taxes, with the number of brackets varying widely by state.

There are 8 states that do not have an income tax, making tax-exemption less valuable. Those states include Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming.

Certain issuers of tax-exempt bonds have their bond’s interest triple tax-exempt no matter where the buyer lives. Those issuers are Puerto Rico, Guam, Virgin Islands, Northern Mariana Islands and American Samoa.

Washington, DC does not tax in-state or out-of-state municipal bonds. Residents can buy tax-exempt bonds from an issuer and not pay state or district income taxes on the interest.

4. The bond’s repayment risk (i.e., credit)

Not all issuers have the same risk of repayment of principal and interest in the future.

The credit rating helps the buyer access this risk of the bond at the time of purchase. However, risks can change over time (e.g., COVID constraints reduce many governments revenues) and thus the economics of the bond can change.

Although bonds make fixed rate payments of interest and return the principal at maturity, there is no guarantee of either.

The issues above (except the bond’s repayment risk) help the buyer calculate the taxable yield equivalent of their tax-exempt bond (or visa-versa).

Determining the Economics

The issues above (except the bond’s repayment risk) help the buyer calculate the taxable yield equivalent of their tax-exempt bond (or visa-versa).

The theoretical ratio between tax exempt and taxable bonds is based on the tax rate of the purchaser. If the purchaser’s tax rate is 37%, then the breakeven point where the purchaser would be indifferent would be 63% (tax exempt rate of 3.15% and taxable rate of 5%).

If this tax exempt/taxable ratio is above 63%, then the tax-exempt bond has a better after-tax return. Conversely, if the ratio is below 63%, the taxable bond has a better after-tax return.

Let's assume a person in Minneapolis, MN purchased a $10,000 5% coupon State of Minnesota tax-exempt bond at par (e.g., price =$100), and their tax brackets were as follows:

- 30% federal tax bracket

- 7% state tax bracket

- 1% local tax bracket

The taxable equivalent of the bond would be 8.06%:

However, if the same person purchased a $10,000 5% State of New York tax-exempt bond at par (e.g., price =$100), the taxable equivalent of the bond would be 7.14%.

There are two other variables to think about when analyzing the economics of buying a tax-exempt bond:

- Other potential investments (don’t forget taxable equivalent as a current way to compare tax-exempt and taxable)

- The yield spread between a taxable bond (e.g., a treasury bond) and a tax-exempt bond (e.g., AA- credited tax-exempt bond)

Other potential investments

Fixed income securities have a fixed return (if everything goes as planned) which means other investments can potentially have higher returns, but carry more risk (e.g., equity market securities). Although not measurable analytically, unless using historical trends, a tax-exempt bond may or may not have a better return depending on market conditions.

Market spreads

There is always a spread between taxable securities (e.g., US Treasury, Corporate bonds) and tax -exempt securities.

This spread moves depending on current risk levels, current market supply/demand levels, and length of the maturity of the security.

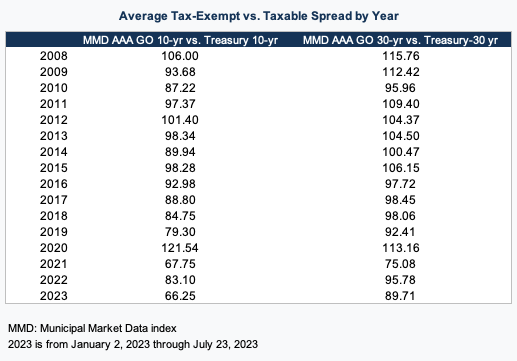

Back in the 1990’s, the spread ranged from 75% to 80% (approximately). As an example, the buyer of a fixed rate security in the open market could have purchased either a 5.00% taxable yielding bond or a 3.75% yielding tax-exempt security (assumes both have the same credit risk/rating).

Depending on their tax bracket, one could have yielded to the buyer more than the other.

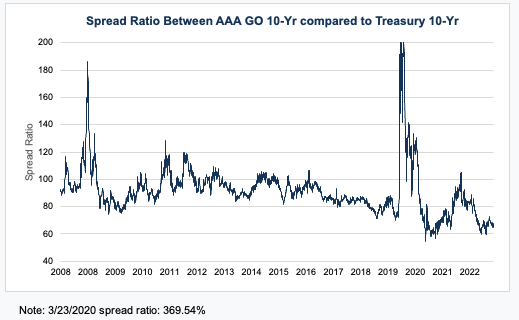

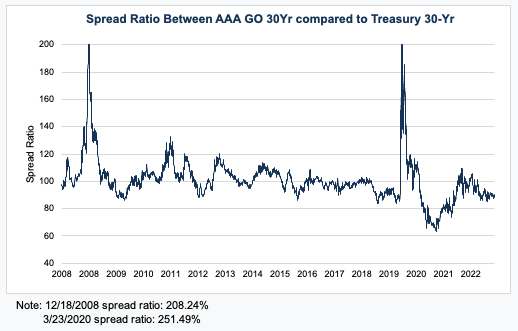

During the 2007/2008 economic crisis, and for a short period in 2020 due to COVID, the spread was over 100% due to the lack of interest in purchasing tax-exempt bonds (due to the economic losses and lack of need of tax-exempt income).

In this case, the buyer of a fixed rate security in the open market could have purchased either a 5.00% taxable yielding bond or a 5.20% yielding tax-exempt security (assumes a spread of 1.04% and that both securities have the same credit risk/rating).

The table below shows the current and 10-year historical spreads for 10-year and 30-year securities:

Conclusion

The economics of a tax-exempt security can be different for any potential buyer. There is a simple tax-exempt to taxable bond yield equivalent calculation that somewhat summarizes the economics in simplistic terms.

However, a deeper look into the bond equivalent calculation shows that many components must be independently analyzed at the date of purchase of the bond, including, but not limited to:

- Issuer of bond

- General market conditions

- Spreads between tax-exempt and taxable bonds

- Credit worthiness of the issuer

Even with this information, future changes in the issuer’s credit or changes in the markets in general also affect the economics of a tax-exempt bond.

One additional thought: the selling of bonds can produce either an economic gain or loss. From an accounting perspective, these gains or losses are seen as ordinary income so there is no tax-exemption on either the gain or loss.

Gains or losses are capital gains as long as the discount when purchased does not cause the de minimis penalty (i.e., more discount than 0.25% per year to maturity from date of purchase.)

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)