Rising interest rates affect both new municipal bond issuances and refunding opportunities. Even a 0.25% rate increase can significantly raise project costs or eliminate refinancing savings.

In this blog, we explain how higher rates impact financing structures and provide examples to illustrate the long-term budgetary effects.

Learn how municipal issuers can adapt to a changing rate environment.

Understanding the Impact of Federal Rate Increases on Municipal Borrowing

Over the past 24 months, in order to battle inflation, the Federal Reserve has been increasing the Federal Funds Rate.

This rate is used as a part of the “calculation” to set interest rates on most municipal issuances.

From the issuer’s perspective, the increase in interest rate affects current and future issuances of municipal debt. The volatility does affect existing bond holders, in that the value of their bonds decrease when interest rates rise, but this does not directly affect the municipal budget.

The two main types of debt issuances, new project financings and refunding financings, are impacted differently.

How Do Rising Rates Affect New Municipal Projects?

The higher the interest rates, the more costly the financing of a new project is over the long run, thus increasing pressure on the municipal budget.

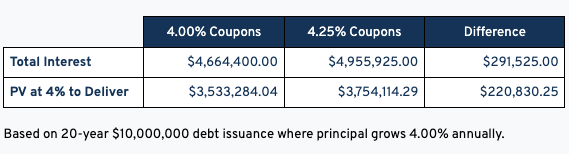

As a simple example, below we compare a $10,000,000 level debt service municipal financing at different rates.

- Example 1: 4.00% coupon rates, sold at par, with serial bonds that mature annually from year 1 to year 20.

- Example 2: The same $10,000,000 financing with 4.25% coupon rates, sold at par, with serial bonds that mature annually from year 1 to year 20.

The results displayed above show that an increase of just 0.25% on the bonds used to finance the project will cost the issuer an additional 6.25% in interest over the life of the 20-year financing, or in today’s dollars, an additional $220,830.25. (Please note: the results will differ depending on the structure of the bond financing, e.g., level debt, deferred principal payments, etc.)

Why Refunding Become Less Attractive as Rates Rise

The higher the bond yield environment, the less cash flow savings the refunding financing will achieve.

The yield and the coupon on a bond drive the price of the bond. As yield and price are inversely related, if the yield of a bond increases, the price decreases, and vice versa.

In a high yield environment, an issuer has to sell more bonds to generate the necessary proceeds to fund an escrow (which pays off the old bonds), thereby decreasing the potential economics a refunding can produce when compared to a lower rate environment.

Refunding economics are based on replacing an existing transaction’s cash flow (the principal and interest payments of the “refunded” bonds) with a transaction with a lower cash flow (the “refunding” bonds).

If the refunded bonds were sold in a higher coupon/yield environment than the refunding bonds, based on the structure of the refunding bonds (e.g., level annual savings), the annual interest payments made by the issuer would be reduced thus producing future cash flow savings and budgetary relief.

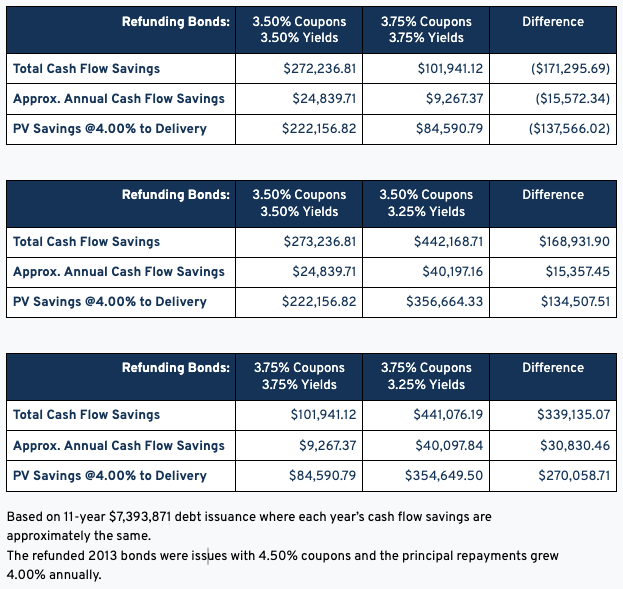

To show how both the coupons and the yield define the cash flow savings achieved from a refunding, below we compare refunding an outstanding $100,000,000 Series 2013 transaction with 10 years left until final maturity (initially issued with 4.50% coupons) with:

- A refunding transaction with 3.50% coupons/3.50% yields and a refunding transaction with 3.75% coupons/3.75% yields.

- A refunding transaction with 3.50% coupons/3.50% yields and a refunding transaction with 3.50% coupons/3.25% yields.

- A refunding transaction with 3.75% coupons/3.75% yields and a refunding transaction with 3.75% coupons/3.25% yields.

The results above display that the savings achieved by the refunding are drastically reduced by a 25bp (0.25%) change in the coupon on the refunding bonds (assuming the refunding bonds are to be sold at par).

Note that the savings increase with the same refunding bond coupon when that bond has a lower yield.

If the refunding bonds were sold at 3.80% coupons/yield, there would be no future savings produced by the refunding bonds. The results also show that the lower the refunding bond’s yield, the more savings produced.

You’ll notice the refunding bonds sold at 3.50% coupon/3.25% yield and 3.75% coupon/3.25% yield produce close to the same savings. This is due to the high price of the 3.75% coupon/3.25% yield bonds.

Conclusion

In summary, even the smallest change in interest rates/yields can have a large effect on:

- How much a project will cost an issuer

- The economics achievable by a refunding (refinancing) of an already outstanding transaction

As interest rates increase/yield increase, issuers must decide if the economics of projects are feasible, whether being paid off with future tax revenues or project revenues.

On the refinancing front, the economics of a refunding must produce savings, or the issuer will have to continue paying off the existing outstanding bonds until maturity.

Frequently Asked Questions

Q: How do rising interest rates affect municipal bond issuers?

A: Rising interest rates increase the cost of borrowing for new municipal projects and reduce the potential savings from refunding outstanding bonds. Issuers must carefully evaluate the financial impact before proceeding with new debt.

Q: What is the Federal Funds Rate and why does it matter for municipalities?

A: The Federal Funds Rate influences overall interest rates in the economy, including those applied to municipal bonds. When the rate rises, it typically leads to higher borrowing costs for municipal issues.

Q: What's the difference between new project financings and refundings in a high-rate environment?

A: New financings become more expensive, increasing long-term interest costs. Refunding opportunities, which depend on achieving lower interest costs, often disappear when rates rise.

Related Municipal Finance Reading

- DebtBook's Premium/Discount Amortization Methodology Explained

- DebtBook’s Guide to the Incremental Borrowing Rate

- McHenry County, IL, Leverages ‘Hidden Gem’ DebtBook to Simplify Debt Schedules and Financial Statements

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)