If you're a public sector organization with a fiscal year beginning after June 15, 2022, the time to comply with GASB 96 has arrived.

Ideally, you're well on your way toward maintaining segmented records for all ongoing subscription-based information technology arrangements (SBITAs). But in reality, you're probably busy juggling a dozen other financial reporting obligations and haven't gotten around to setting up a system for complying with GASB 96.

We understand.

That's why we pulled together this guide to help you understand one specific part of GASB 96: capitalized project costs.

GASB 96: What are SBITAs?

Understanding SBITAs & why they matter

Definition:

Subscription-based information technology arrangements, or "SBITAs," are related to subscription payments made by a public sector organization for the rights to use a vendor's software system.

The Governmental Accounting Standards Board released GASB 96 as a follow-up to GASB 87, which provided guidance on how governmental bodies should account for leases.

GASB 96 supports the goal of accurate financial reporting by creating a uniform definition and treatment of SBITAs, leading to consistency and comparability across governmental bodies.

Finally, GASB 96 provides guidance on accounting treatment for the individual components of SBITAs. The remainder of this article will focus on one of these components: project costs.

What are GASB 96 project costs?

Definition:

Project costs are cash outlays for activities associated with selecting, implementing, and maintaining SBITAs. Project costs are in addition to subscription payments.

The intangible asset value of SBITAs equals the present value of lifetime subscription payments plus capitalized project costs.

Now, determining the lifetime value of subscription payments is the easy part of the equation — it's in the contract with your SBITA vendor. The tricky part is what we're focusing on: identifying capitalizable project costs.

To do this, you must understand the following two components of SBITA projects and their associated costs:

- Stages in a project's life cycle

- The accounting treatment of costs in each stage

Let's start with point one, "Stages in a project's life cycle."

Project stages

The activities associated with a SBITA should be grouped into three stages:

- Preliminary stage

- Initial implementation stage

- Operational and additional implementation stage

Preliminary stage costs

Cash outlays in the preliminary stage of a project include all activities that ultimately lead to the final selection of the technology and SBITA vendor.

For example, during the preliminary stage of a SBITA project, an organization may incur costs related to evaluating various vendors and technologies, defining system requirements, and picking a vendor.

Once a vendor is selected, the project moves into the initial implementation stage.

Initial implementation stage costs

Cash outlays in the initial implementation stage of a project include all ancillary charges necessary to place the subscription asset into service.

For example, during the initial implementation stage of a SBITA project, an organization may incur design, configuration, coding, testing, and installation-related costs incurred by internal IT teams or advisors/consultants assisting with the implementation of the software. Initial implementation activities may also include data migration from an old system to the new one.

The commencement of the subscription term occurs at the completion of the initial implementation stage. At this time, your organization has obtained control of the right to use the underlying IT assets; therefore, the subscription asset is in service.

The project now moves into the operational and additional implementation stage.

Understand our implementation process at DebtBook.

Operational and additional implementation stage costs

Cash outlays in the operational and additional implementation stage relate to the maintenance of the system and other activities necessary for an organization's ongoing operations related to the SBITA.

For example, during the operational and additional implementation stage of a SBITA project, an organization may incur costs related to system updates.

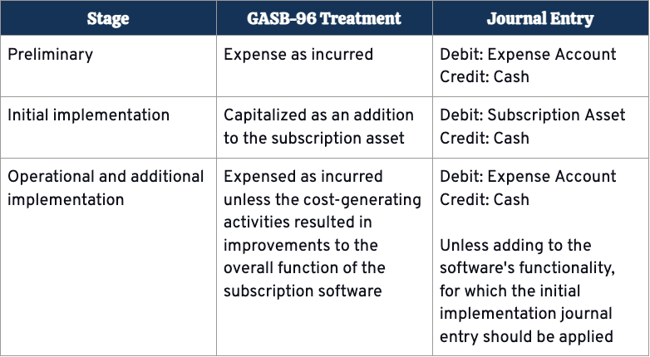

Treatment of costs incurred in each stage of a project

Once you know the costs associated with each project stage, the next step is to accurately account for these costs.

The table below summarizes the treatment of costs in each stage and provides the requisite journal entry.

Tip:

All costs incurred from training employees on how to use the subscription software are treated as expenses, regardless of the stage in which the training occurred.

Accounting for GASB 96 subscription project costs

Unfortunately, system implementation is not always a linear process. For instance, it's likely not possible to state that Days 1–20 were preliminary stage costs, Days 21–40 were initial implementation stage costs, and all days after were operational stage costs.

Instead, an organization may incur costs across multiple stages at once, leaving them with the tedious job of working through the following process:

Identifying and recording project costs

To begin, collect all cash outlays and, for each of them, answer the following questions:

- Does the cost relate to a SBITA?

- If yes, proceed to the next question.

- If no, the cost falls outside GASB 96 regulations.

- Is the expense a preliminary stage cost?

- If yes, record the cost as an expense.

- If no, proceed to the next question.

- Is the cost an implementation cost?

- If yes, capitalize the cost and record the cash outlay as an increase to the subscription asset.

- If no, proceed to the next question.

- Is the cost related to an operations activity that improved the system's functionality?

- If yes, capitalize the cost and record the cash outlay as an increase in the subscription asset.

- If no, record the cost as an expense.

Next, using the bucketed cost data collected in the previous step, prepare and record the necessary journal entries to book the subscription asset.

Finally, after the initial recording of the asset and for the duration of the subscription term, calculate the amortization and interest expenses, and prepare the necessary journal entries to record these amounts.

Let's take a look at what this process looks like in practice.

Project costs example

The World County Parks and Recreation Department needs a new recreation management system.

Facts

The department begins by defining its requirements for the system, such as facility management portals, event management, sports league management, and the ability to collect fees and waiver forms from the community. Next, the team meets with various software vendors to discuss their products before selecting Software A.

The parties agree to a three-year subscription term at $500 a month at 2% interest, for a total present value subscription liability of $12,744.

Throughout this process, the team working on a project spends $1,500 on employee travel, lodging, and meals while visiting potential vendors.

Next, the department dedicates two internal IT employees to install and configure the software to align with the specific needs of World Parks and Recreation. The employees each make $30/hour, and installation takes 55 hours.

Two months after the installation, the same IT employees execute a system update. The update takes 5 hours.

Classifying Project Costs

Based on the presented facts, the World Parks and Recreation Department incur the following costs related to the Recreation Management Software project.

- Monthly subscription payments of $500

- Employee costs related to selecting a SBITA vendor ($1,500)

- Employee costs incurred while installing the software ($3,300)

- Employee costs associated with executing a system update ($300)

The selection of the vendor and system update costs would be considered preliminary stage and operations stage costs, respectively, qualifying the costs as expenses.

Calculation of Subscription Asset

Remember, the book value of a subscription asset equals the present value of lifetime subscription payments (the subscription liability) plus capitalized project costs.

We know the subscription liability is $12,744, and capitalized initial implementation costs amount to $3,300.

So, the value of the recreation management subscription asset is $16,044 with a monthly amortization rate of $446 ($16,044/36 months).

Journal Entries

Initial entry to record the subscription asset and corresponding subscription liability:

Gross Subscription Asset 16,044

Subscription Liability 12,744

Cash 3,300

Monthly journal entries thereafter:

Amortization Expense 446

Subscription Liability 500

Accumulated Amortization 446

Cash 500

Tip:

Is the SBITA related to a government fund that uses the modified accrual accounting method? If so, the balance must be converted at year-end using the full accrual method to prepare financial statements.

Preparing for GASB 96 compliance

The introduction of GASB 96 adds complexity to your already complicated accounting processes. As a result, it's easy to get overwhelmed or fall behind on your compliance requirements.

DebtBook can help.

DebtBook allows you to not only manage the subscription payments themselves but also identify and track capitalized project costs with GASB 96 software. Plus, thanks to automatic uploads of capitalized costs, rather than you searching through your GL to determine what counts as SBITA, what's capitalizable, etc., DebtBook can help categorize your costs for you.

Download the resource below to find a list of common GASB 96 subscription types.

Related reading:

- SBO Perspectives Podcast – "GASB 96: Take a “Byte” out of SBITA"

- Building An Action Plan For GASB 96 Compliance

- Planning & Preparing for GASB 96

Disclaimer: DebtBook does not provide professional services or advice. DebtBook has prepared these materials for general informational and educational purposes, which means we have not tailored the information to your specific circumstances. Please consult your professional advisors before taking action based on any information in these materials. Any use of this information is solely at your own risk.

.jpg)

.jpg)

.jpg)